Securing an FHA loan pre-approval is a critical first step for many first-time homebuyers, offering a clear path toward realizing their homeownership dreams. This comprehensive guide simplifies the process, empowering you to navigate the complexities with confidence and increase your chances of a successful home purchase.

Toc

- 1. The Benefits of FHA Loan Pre-Approval

- 2. Preparing Your Finances for FHA Loan Pre-Approval

- 3. Related articles 01:

- 4. Navigating the Pre-Approval Process

- 5. Related articles 02:

- 6. Preparing for a Smooth Closing

- 7. Addressing Common Concerns and Misconceptions

- 8. Conclusion: Unlocking Your Homeownership Dreams

Contrary to popular belief, FHA loans are not just for low-income borrowers. These flexible mortgage options are accessible to a wide range of individuals, provided they meet the eligibility criteria. The FHA home loan pre-approval process is designed to assess your financial readiness, give you a realistic budget, and make you a more attractive buyer in a competitive market.

The Benefits of FHA Loan Pre-Approval

Before diving deeper into the process, let’s explore the benefits of obtaining an FHA loan pre-approval. Understanding these advantages can motivate you to get started and help you make informed decisions throughout your home-buying journey.

-

Establishing a Realistic Budget: FHA loan pre-approval provides clarity on how much you can borrow, allowing you to set a realistic budget for your home search. This insight enables you to focus on properties within your price range, saving you time and effort.

-

Strengthening Your Offer: In a competitive housing market, a pre-approval letter shows sellers that you are a serious buyer. It demonstrates your financial capability and reduces the seller’s risk, often leading to a higher likelihood of your offer being accepted compared to those without pre-approval.

-

Streamlining the Buying Process: With pre-approval, you have a head start on the mortgage process. You’ll have a clear understanding of the documents required, making the overall home-buying process smoother and faster.

-

Identifying Potential Issues Early: The pre-approval process involves a thorough review of your financial situation. For example, if your debt-to-income ratio is too high, the pre-approval process might reveal this early, allowing you to explore options like paying down debt or finding a less expensive home before wasting time searching for properties beyond your financial reach. Some lenders might also offer financial counseling to help borrowers improve their financial situation before proceeding with a loan application.

-

Competitive Advantage: In a hot real estate market, homes can sell quickly. Having a pre-approval letter allows you to act fast when you find a property you love, giving you a competitive edge over other buyers who may still be in the pre-qualification stage. However, even with pre-approval, the buyer might still lose out on a desirable property to a cash buyer or another buyer with a significantly stronger offer.

Preparing Your Finances for FHA Loan Pre-Approval

One of the key aspects of the “FHA loan pre-approval” process is assessing your financial situation. This involves calculating your debt-to-income (DTI) ratio, which lenders typically prefer to be 43% or lower. Additionally, it’s crucial to review your credit report and dispute any errors to ensure a strong credit profile.

Understanding Your Financial Readiness

-

Calculating Your Debt-to-Income Ratio: Your DTI ratio compares your monthly debt payments to your monthly gross income. To calculate your DTI, add up all your monthly debt payments (including credit cards, student loans, and any other loans) and divide that sum by your gross monthly income. For example, if your monthly income is $5,000 and your total monthly debt payments are $2,150, your DTI would be 43%. Lenders typically look for a DTI ratio of 43% or lower, although some may allow for higher ratios under certain circumstances.

1. https://goldnews24h.com/archive/5114/

2. https://goldnews24h.com/archive/5117/

3. https://goldnews24h.com/archive/5165/

-

Understanding Credit Score Requirements: The minimum credit score for an FHA loan with a 3.5% down payment is 580. If your score falls between 500 and 579, you may still qualify, but you’ll need to make a larger down payment of at least 10%. Improving your credit score can significantly enhance your chances of approval and may even lead to a lower interest rate, resulting in substantial savings over the life of the loan.

-

Reviewing Your Credit Report: Before applying for pre-approval, obtain a copy of your credit report from all three major credit bureaus: Experian, TransUnion, and Equifax. Review it for any inaccuracies or errors and dispute them if necessary. Paying down existing debts and making timely payments can also help boost your credit score.

-

Saving for a Down Payment: While the minimum down payment for an FHA loan is 3.5%, saving for a larger down payment can improve your loan-to-value ratio and strengthen your application. A higher down payment may also help you secure a lower interest rate, which can save you money over the life of the loan.

-

Estimating Closing Costs: Don’t forget to factor in closing costs when budgeting for your home purchase. These costs typically range from 2-5% of the loan amount and may include appraisal fees, title insurance, and various other fees. Understanding these upfront expenses will help you budget accordingly and avoid any unpleasant surprises.

Gathering Necessary Documents

To ensure a smooth “FHA home loan pre-approval” process, you’ll need to gather several key documents, including:

- Government-issued ID: A valid photo ID, such as a driver’s license or passport.

- Social Security number: Required for credit checks and identification.

- Pay stubs: Provide your pay stubs for the last two months to verify your income.

- Tax returns: Submit your tax returns for the last two years to demonstrate your financial stability.

- Bank statements: Include bank statements for the last two months to show your savings and assets.

- Details of outstanding debts: List any existing loans, credit cards, and other debts you currently have.

Providing accurate and complete documentation can help expedite the pre-approval process and demonstrate to the lender that you are a responsible and organized borrower.

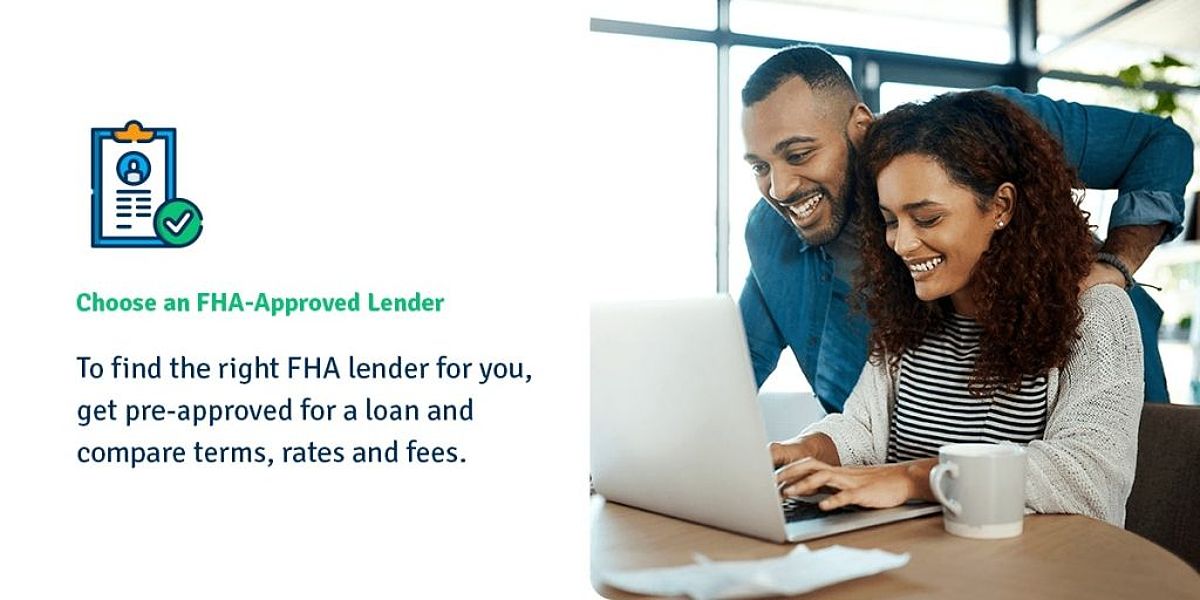

Choosing the Right Lender

Selecting a reputable lender who specializes in FHA loans is crucial. Look for a lender with a proven track record of successful “pre-approved FHA loan” applications and a deep understanding of FHA loan requirements. Compare rates, fees, and customer service to find the best fit for your needs. Don’t hesitate to ask for recommendations from friends or family who have recently gone through the process.

Submitting Your Application

The application process typically involves completing the Uniform Residential Loan Application (URLA/Fannie Mae Form 1003), which covers your financial information, employment history, and the property you’re interested in purchasing. Be prepared to provide accurate and detailed information to ensure a smooth application process.

Lender Review and Feedback

During the review process, the lender will thoroughly examine your credit, income, and assets to determine your eligibility for an FHA loan. They may request additional information or documentation if needed. This meticulous evaluation is what distinguishes pre-approval from the more basic pre-qualification process.

Receiving Your Pre-Approval Letter

If you meet the lender’s FHA loan requirements, you’ll receive a pre-approval letter detailing the loan amount, terms, and any applicable conditions. While this is not a final approval, it’s a strong indication of your eligibility and can make you a more attractive buyer in a competitive market. The pre-approval letter serves as a powerful tool in your home-buying journey, demonstrating to sellers that you are a serious and qualified buyer.

1. https://goldnews24h.com/archive/5117/

2. https://goldnews24h.com/archive/5111/

3. https://goldnews24h.com/archive/5156/

Preparing for a Smooth Closing

After receiving your FHA loan pre-approval, it’s essential to maintain your financial stability to avoid jeopardizing the loan. The next stages of the process include house hunting, making an offer, a home appraisal, final loan approval, and closing. Remember that while pre-approval significantly increases your chances, it’s not a guarantee of final loan approval. Staying financially responsible throughout the process is crucial to ensure a successful home purchase.

House Hunting and Making an Offer

With your pre-approval letter in hand, you can start house hunting with confidence. Work with a knowledgeable real estate agent who understands your needs and can help you find the right property. Once you find a home you love, you’ll need to make an offer. Your real estate agent can assist you in crafting a competitive offer that takes into account the current market conditions. However, even with pre-approval, the buyer might still lose out on a desirable property to a cash buyer or another buyer with a significantly stronger offer.

Home Appraisal and Final Loan Approval

Once your offer is accepted, the lender will require a home appraisal to determine the property’s value. This step is crucial, as the home must meet certain health and safety standards to qualify for an FHA loan. If the appraisal comes in lower than the purchase price, you may need to renegotiate the terms with the seller or consider walking away from the deal.

After the appraisal, the lender will conduct a final review of your financial situation and the property before issuing final loan approval. This process may involve verifying your employment and income again, so it’s essential to maintain your financial stability during this period.

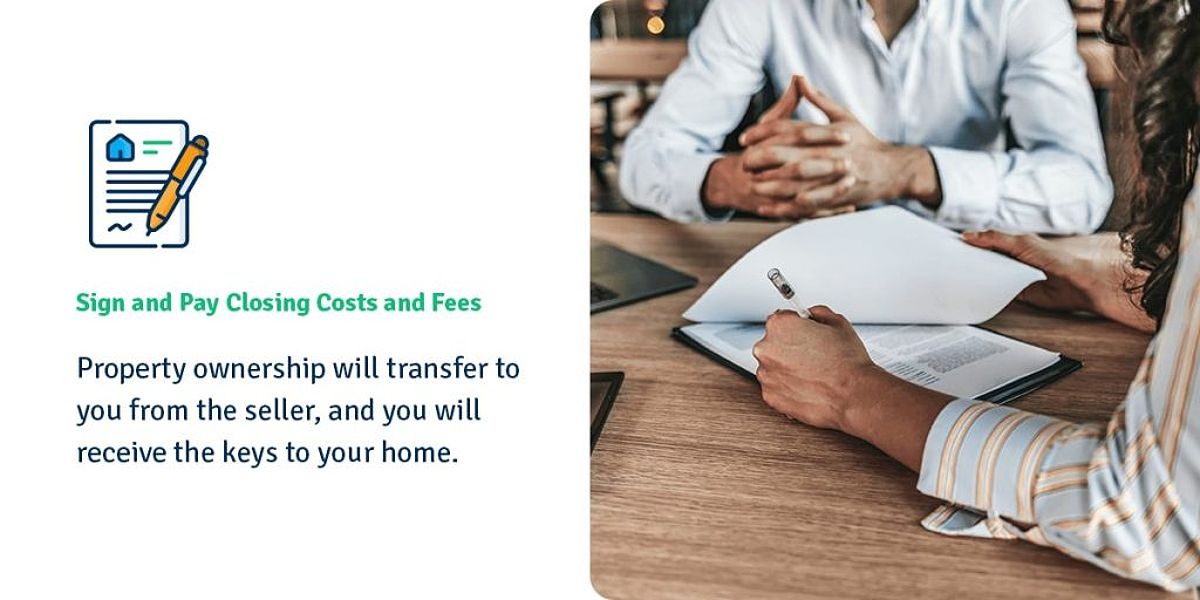

Closing Process

The closing process involves signing the final paperwork and transferring ownership of the property. Be prepared to pay closing costs at this stage, which may include various fees associated with the loan and the purchase of the home. Once everything is signed and the funds are transferred, you’ll receive the keys to your new home!

Addressing Common Concerns and Misconceptions

One common misconception about FHA loans is that they are only for low-income borrowers. In reality, FHA loans are a valuable tool for many first-time homebuyers, regardless of income level, as long as they meet the eligibility requirements. The key is to manage your finances responsibly throughout the “FHA loan pre-approval” process.

Another misconception is that FHA loans are more challenging to obtain than conventional loans. While FHA loans have specific requirements, such as a minimum credit score and down payment, the flexibility of the program makes it accessible to a wide range of borrowers, including those with average credit or limited funds for a down payment.

It’s important to note that the recent increase in interest rates has impacted affordability and competitiveness in the housing market. While FHA loans can still be beneficial for first-time homebuyers, higher interest rates might necessitate larger down payments or more stringent budgeting.

Conclusion: Unlocking Your Homeownership Dreams

Securing FHA loan pre-approval is a crucial step towards achieving your homeownership goals. By understanding the “FHA loan pre-approval” process, preparing your finances, and gathering the necessary documents, you’ll be well-equipped to navigate this journey with confidence. Remember to choose a reputable lender, maintain financial stability, and stay organized throughout the process. Start your pre-approval application today and take the first step toward owning your dream home!